PC Outlook Remains Subdued, According to IDC

PC Outlook Remains Subdued Despite Some Gains In Mature Markets, According to IDC

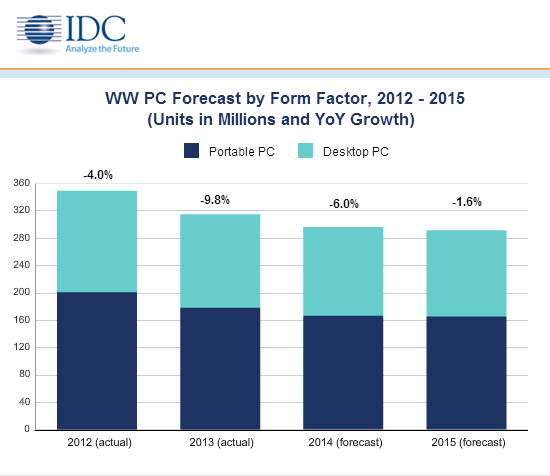

FRAMINGHAM, Mass., June 3, 2014 Worldwide PC shipments are expected to fall -6.0% in 2014, a slight adjustment from the previous forecast of -6.1%, according to the International Data Corporation (IDC) Worldwide Quarterly PC Tracker. Mature regions benefitted primarily from a recovery surge in Western Europe while other mature regions performed modestly above expectations in the first quarter of 2014 (1Q14). Emerging regions continued to see weak demand and difficult conditions, although the economic environment in Latin America had the largest impact. The impact to emerging regions a cornerstone of long-term market stability outweighed the short-term boost seen in mature regions. As a result, longer-term growth was lowered slightly (by less than a percent for 2015-2017), with 2015 at -1.6% year on year with subsequent years still between 0 and -1% growth.

Positive factors for the PC market include slowing tablet demand and steadying economic indicators that are contributing to more stable PC shipments in mature markets. The Windows XP replacement activity that boosted shipments in the past several quarters is also expected to remain a positive factor for a few more quarters. This relative improvement in the outlook will enable the United States to further its lead in PC shipments over China and keep the mantle as the biggest PC market globally through 2017.

Despite the pockets of opportunity, weakening growth in emerging regions and continuing pressure from other devices primarily smartphones and tablets continue to push down the long-term outlook. Consumer interest in PCs remains constrained and price-sensitive, as evidenced by overall market declines and still modest ultraslim notebook results, even as Chromebook vendors and channels expand and boost volume in this low-end segment. The competitive environment is also evidenced in the sale of Sony’s PC division, and Samsung refocusing its PC operations. IDC expects further market restructuring and consolidation going forward as vendors review limited PC growth and look at broader mobility and computing trends.

“PC shipments are currently benefitting from a lull in tablet demand due to rising tablet penetration in mature regions and competitive pressure on smaller tablets from large-size smartphones (sometimes referred to as Phablets),” said Loren Loverde, Vice President, Worldwide PC Trackers. “However, the transition toward mobile and cloud-based computing is unstoppable. PCs continue a slow transition toward touch and slim designs, even as tablet volume is expected to pass total PC volume in the fourth quarter of 2014 and on an annual basis in 2016. To return to growth, the PC industry is going to need to accelerate the shift to lower-cost, thin, and touch-based designs, despite the challenges it has faced with these designs in the past.”

“2014 represents an important shift for the PC market in emerging regions,” said Jay Chou, Senior Research Analyst, Worldwide PC Trackers. “Shipments in these parts of the world are expected to contract in double digits (nearly 20 million units fewer) compared to 2013. Political and economic instability in many of these markets are key factors affecting short-term intake, but a fundamental shift toward computing across the device spectrum represents a broader transition. IDC still expects refresh projects and continued growth in underserved areas to bring modest growth in emerging markets by 2016, but the overall volume has been further curtailed to less than 165 million units per year through the forecast horizon.”

PC Shipments by Region and Form Factor, 2013-2018 (Shipments in millions)

Region

Product Category

2013

2014*

2018*

Emerging Markets

Desktop PC

85.7

79.2

76.0

Emerging Markets

Portable PC

96.2

83.8

87.9

Emerging Markets

Total PC

181.9

163.0

164.0

Mature Markets

Desktop PC

51.1

50.5

43.0

Mature Markets

Portable PC

82.2

82.8

80.4

Mature Markets

Total PC

133.2

133.3

123.4

Worldwide

Desktop PC

136.7

129.7

119.0

Worldwide

Portable PC

178.4

166.6

168.3

Worldwide

Total PC

315.1

296.3

287.3

Source: IDC Worldwide Quarterly PC Tracker, May 2014

* Forecast data

See Table and Taxonomy Notes below.

PC Shipment Growth by Region and Form Factor, 2013-2018

Region

Product Category

2013

2014*

2018*

Emerging Markets

Desktop PC

-9.6%

-7.6%

-0.9%

Emerging Markets

Portable PC

-12.9%

-12.9%

2.2%

Emerging Markets

Total PC

-11.3%

-10.4%

0.7%

Mature Markets

Desktop PC

-4.8%

-1.1%

-2.2%

Mature Markets

Portable PC

-9.3%

0.7%

-1.1%

Mature Markets

Total PC

-7.6%

0.0%

-1.5%

Worldwide

Desktop PC

-7.8%

-5.1%

-1.4%

Worldwide

Portable PC

-11.3%

-6.6%

0.6%

Worldwide

Total PC

-9.8%

-6.0%

-0.2%

Source: IDC Worldwide Quarterly PC Tracker, May 2014

* Forecast data

Table Note: Mature Markets include U.S., Western Europe, Japan, and Canada. Emerging Markets includes Asia/Pacific (excluding Japan), Latin America, Central and Eastern Europe, Middle East, and Africa.

Taxonomy Note: PCs include Desktop, Mini Notebook and other Portable PCs which possess non-detachable keyboards, and do not include handhelds or Tablets such as the Apple iPad, Microsoft Surface Pro or Android Tablets

IDC’s Worldwide Quarterly PC Tracker gathers PC market data in more than 80 countries by vendor, form factor, brand, processor brand and speed, sales channel and user segment. The research includes historical and forecast trend analysis as well as price band and installed base data. For more information, or to subscribe to the research, please contact Kathy Nagamine at 650-350-6423 or [email protected].

About IDC Trackers

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. IDC helps IT professionals, business executives, and the investment community to make fact-based decisions on technology purchases and business strategy. More than 1,000 IDC analysts provide global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. In 2014, IDC celebrates its 50th anniversary of providing strategic insights to help clients achieve their key business objectives. IDC is a subsidiary of IDG, the world’s leading technology media, research, and events company. You can learn more about IDC by visiting www.idc.com.